Breaking Down Your Personal Auto Policy: Terms Every Driver Should Know

Reading Time: 4-5 Minutes

Key Takeaways

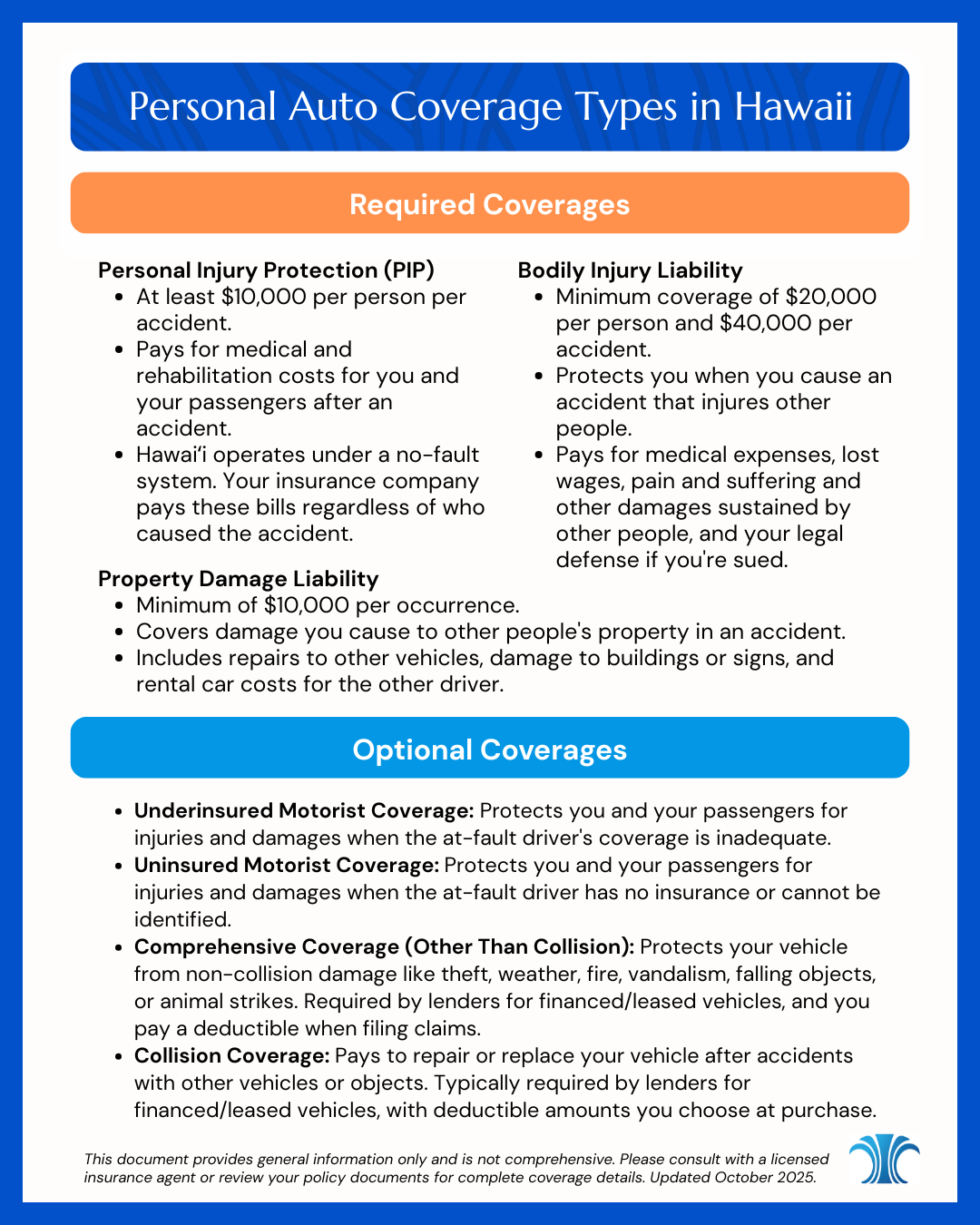

- Hawai'i requires coverage for Personal Injury Protection (PIP) ($10,000 per person per accident), Bodily Injury Liability ($20,000 per person/$40,000 per accident), and Property Damage Liability ($10,000 per accident).

- Hawai'i also requires insurers to offer Uninsured Motorist and Underinsured Motorist Coverages at the same limits required for Bodily Injury Liability Coverage.

- For new policies or policies renewing after January 2026, the minimum limits for Bodily Injury Liability, Uninsured Motorist and Underinsured Motorist Coverages increase to $40,000/$80,000. Property Damage Liability increases to $20,000 and PIP remains at $10,000.

- Your PIP pays first for medical expenses regardless of who caused the accident.

- "Full coverage" for your vehicle means liability plus Comprehensive (also called Other than Collision) and Collision coverage for your vehicle. Lenders require these for financed cars, and higher deductibles lower your premiums.

If you’re a Hawai'i resident with a vehicle, having auto insurance is required by law. You have auto insurance, but what does everything mean? Understanding your auto insurance policy can help you make better decisions about your coverage to keep you adequately protected on the road.

This guide explains the most important auto insurance terms in simple language. Remember that insurance laws and requirements can change, so verify current information with your insurance agent.

Key Financial Terms Every Driver Should Understand

- Premium: Your premium is the amount you pay for your insurance coverage. Several factors affect your premium cost, including your driving record, the type of car you drive, and your coverage limits and deductibles. Hawai'i law prohibits insurance companies from using credit scores, gender, or race when setting rates [2].

- Deductible: A deductible is the amount you pay out of your own pocket before your insurance coverage begins. Deductibles typically apply to comprehensive and collision coverage. Common deductible amounts are $250, $500, and $1,000.

- For example, you back into a pole and the repair cost is $2,000. If you have a $500 deductible, you must pay $500 out of pocket and your insurance company will then cover the remaining $1,500.

- Higher deductibles mean lower premiums, but you'll pay more out-of-pocket when you file a claim. Choose a deductible amount you can afford to pay if you need to make a claim.

- Policy Limits: Policy limits are the maximum amounts your insurance company will pay for covered losses. Hawai'i's minimum requirements are often written as 20/40/10, meaning $20,000 per person for bodily injury, $40,000 per accident for bodily injury, and $10,000 per occurrence for property damage [1]. Understanding your limits helps you decide if you need more coverage. For all new policies and existing policies renewed on January 1, 2026 or later, the minimum limits will be 40/80/20.

Coverage Types Required in Hawaii

- Personal Injury Protection (PIP): Personal Injury Protection, commonly called PIP, is an important coverage in Hawaii. Hawaii requires at least $10,000 per person in PIP coverage [1]. This coverage pays for medical and rehabilitation costs for you and your passengers after an accident.

- Hawai'i operates under a no-fault system, which means your insurance company pays these bills regardless of who caused the accident. While $10,000 or $20,000 might seem like enough, keep in mind that medical costs can add up quickly.

- To learn more about PIP, click here.

- Bodily Injury Liability: Bodily injury liability coverage protects you when you cause an accident that injures other people. In 2025, Hawai'i required minimum coverage of $20,000 per person and $40,000 per accident [1]. For any policy bound on or after January 1, 2026, minimum coverage of $40,000 per person and $80,000 per accident is required. This coverage pays for medical expenses, lost wages, pain and suffering and other damages sustained by other people and covers your legal defense if you're sued.

- Property Damage Liability: Property damage liability covers damage you cause to other people's property in an accident. In 2025, Hawai'i required a minimum of $10,000 per occurrence [1]. This includes repairs to other vehicles, damage to buildings or signs, and rental car costs for the other driver. Starting on January 1, 2026, Hawai'i will require all vehicles to carry a minimum of $20,000 per accident.

Optional but Important Coverage Types

- Uninsured Motorist (UM) and Underinsured Motorist Coverages (UIM): These coverages pay you and your passengers damages you are legally entitled to recover as a result of bodily injuries or death caused by drivers without insurance (UM) or with inadequate Bodily Injury Liability insurance (UIM). Hawai'i law requires insurance companies to offer these coverages [1]. UM applies when you're injured by an at-fault uninsured driver or when the at-fault driver cannot be identified. UIM coverage applies when the other driver's insurance liability limits are too low. Please note these coverages do not pay for property damage.

- Comprehensive Coverage (also called Other Than Collision Coverage): Comprehensive coverage protects your vehicle from damage not caused by collisions. Coverage includes theft, weather damage, fire, vandalism, falling objects, or if you hit an animal. For example, a woman parks her car outside overnight and wakes the next morning to discover a tree branch fell and shattered her windshield. Comprehensive coverage will help Makiko cover the cost of repairs after her deductible.

If you have a car loan or lease, your lender typically requires this coverage. You'll typically pay a deductible when you file a claim.

- Collision Coverage: Collision coverage pays to repair or replace your vehicle when it's damaged in an accident with another vehicle or object. Lenders require this coverage on financed or leased vehicles. You choose a deductible amount when you buy this coverage.

- Other Coverage: Other optional coverages include but are not limited to: Additional Personal Injury Protection, Death Benefits, Funeral Expenses, Wage Loss Benefits, and more.

Important Policy Features and Processes

- Claims Process: When you need to file a claim, contact your insurance agent or company as soon as possible after the incident. Note the date, time and location, have your policy number, driver's license, and details about the incident ready. Your agent or insurance company will guide you through their specific claims process.

To learn more about the claims process, click here.

- Coverage for Other Drivers: Your auto insurance follows your car, not the driver. This means your policy may provide coverage when someone else drives your car with your permission. However, coverage details can vary, so check with your insurance company about specific restrictions and how claims might affect your rates.

- Full Coverage: "Full coverage" is a common term that doesn't have a specific legal meaning. People often use this term to describe a policy that includes all required liability coverages, plus comprehensive and collision coverages. If you finance or lease your vehicle, your lender will require comprehensive and collision coverages.

Hawai'i-Specific Considerations

Hawai'i's no-fault insurance system means your PIP coverage pays for your medical expenses regardless of who caused the accident. However, you can still be sued for serious injuries or when damages exceed certain thresholds. Hawai'i also has unique challenges like limited repair facilities on some islands and weather-related risks.

Review Your Auto Policy Today

Regular policy reviews ensure your coverage keeps up with changes in your life, such as buying a new car or moving. Review your current policy to see what coverage you have and consider whether your limits meet your needs. If you have questions about your coverage, contact your insurance agent for clarification.

Frequently Asked Questions

Q: What does “full coverage” car insurance actually mean?

A: "Full coverage" for your vehicle means liability plus Comprehensive (also called Other than Collision) and Collision coverage for your vehicle. Lenders require these for financed cars, and higher deductibles lower your premiums.

Q: How does Hawai'i’s no-fault system work?

A: Under Hawai'i's no-fault system, your Personal Injury Protection (PIP) coverage pays for your medical and rehabilitation expenses regardless of who caused the accident. This means your own insurance covers your medical bills first, even if someone else was at fault.

Q: What's the difference between Comprehensive and Collision coverage?

A: Collision coverage pays for damage to your vehicle from accidents with other vehicles or objects. Comprehensive coverage (also called Other Than Collision) protects your vehicle from non-collision damage like theft, weather, fire, vandalism, falling objects, or hitting an animal.

Q: Should I choose a higher or lower deductible?

A: Higher deductibles result in lower premiums, but you'll pay more out-of-pocket when filing a claim. Choose a deductible amount you can comfortably afford to pay if you need to make a claim. Common amounts are $500, and $1,000.

Sources

- Hawaii Department of Commerce and Consumer Affairs. Motor Vehicle Insurance Information. Hawaii Department of Commerce and Consumer Affairs. Accessed September 23, 2025. https://cca.hawaii.gov/ins/consumers/mvi/

- Hawaii State Legislature. Hawaii Revised Statutes, Chapter 431 - Insurance Code. Hawaii State Legislature. Accessed September 23, 2025. https://www.capitol.hawaii.gov/hrscurrent/vol09_ch0431-0435h/hrs0431/HRS_0431-.htm

- National Association of Insurance Commissioners. Consumer Resources. National Association of Insurance Commissioners. Accessed September 23, 2025. https://www.naic.org/consumers.htm

Related Articles